My wife and I worked our way through the kid’s stuff, and now it was time to tackle our piles.

The biggest pile we had were some plastic storage bins full of financial statements.

While we were good at organizing our financial paperwork at first, it slowly got away from us as kids came into the picture.

Now it was to time to start cleaning house.

My wife started on the bin and quickly asked me how long do we need to keep financial records.

I said it depends and then realized it would be best for me to handle this job since I have a better understanding of it.

But then it occurred to me that most people probably wonder as well how long they should keep financial statements.

The sad truth is, it is not a clear cut answer.

There are a lot of exceptions.

If you want to organize your financial paperwork, you came to the right place.

I will detail everything in this post below.

By the end of the post, you will know what to keep, what to shred, and have an organizational plan to keep clutter at a minimum.

Table of Contents

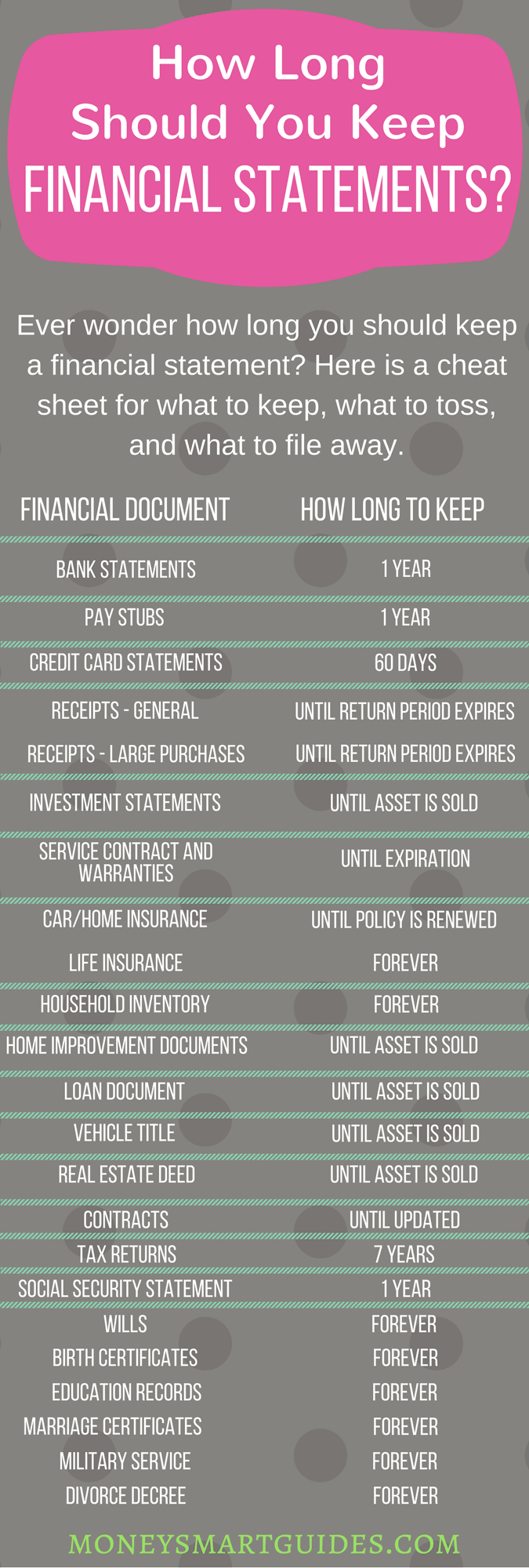

I am going to start off with an important papers checklist so you have a quick idea of what you should keep and what you should shred.

The reason for shredding is to avoid the possibility of someone stealing your identity.

We have been using it for years now.

Before this one, it seemed like we would buy a new one annually. They just broke down.

This one is a beast and has not let us down.

OK, back to the personal record keeping checklist.

This is a general guide for what you need to keep and what you can get rid of.

I encourage you to keep reading as there are some exceptions to the list depending on your personal situation.

Let’s look at each of these in more detail so you can understand if you can shred a financial statement sooner than listed.

We will start with how long to keep bank statements since these financial documents apply to almost everyone.

Each month, you should be reconciling your checkbook to the statement that the bank sends you or you get online.

After you verify everything is correct, you should keep the monthly bank statements for one year.

The exception to this is if there was a purchase made that relates to taxes, home improvements, a business expense, etc.

In these cases, you will want to hold on to the statement permanently, or until you sell the house, business, etc.

Some readers may be wondering if they have online access to their statements through online banking, why the need to keep the paper copy?

After all, the bank can get them for you.

While this is true, most banks will only offer you electronic records back to a certain time, say two years.

Anything older is considered “research” and they charge you per the hour for this. The average charge is $25 an hour.

And while it should only take a few minutes to pull up your account history, who is to say it won’t take them a few hours because of the “complexity” of your account history?

The simple solution is to save the statements, avoid the fee.

The length of time for keeping canceled checks varies.

If you paid by check at the grocery store, you can shred the canceled check after you get your monthly statement.

Same goes for any other checks that have cleared and are not part of a larger purchase.

By larger purchase I mean any of the following:

These cancelled checks should be kept until they are no longer needed.

For example, you would keep any cancelled checks related to tax payments or charitable donations for 7 years, since the IRS can go back that far with an audit.

For a canceled check that paid your mortgage, you would keep until you pay off the house.

For a cancelled check on a flat screen TV, you keep it for a year or two until the warranty expires.

You can shred receipts once you verify your bank or credit card statement is correct, or the warranty or return period has passed.

For receipts that relate to home or business expenses, you will want to hold onto those until you sell the house or business.

Also you want to keep any receipt that can be used for tax purposes, so you have a paper backup in case the IRS comes calling.

For receipts you plan to hold on to for a long time, like home or business expenses, you might want to consider scanning them into a digital file.

This is because over time, the ink on the receipts tends to fade and a blank receipt isn’t going to do you much good.

Another option would be to take a picture of the receipt so you have a copy of it.

Keep your monthly bills, like utility bills (electric, water, sewer), cable and internet, etc. for one year.

After that, you can shred them.

In the event the bill is tax related, like if you run a business out of your house, you will want to keep those bills for 7 years, again just in case you get audited.

Another bill to keep is if it was for a large purchase and you need proof of purchase for a warranty claim.

You should keep the receipt for anything you purchase with your credit card until the statement arrives.

Once you verify they match and the return period on the item has passed, you can toss the receipts.

If there is a tax related purchase, you should keep the statement for 7 years.

Otherwise, there is no need to keep the statement any longer than 60 days.

As with banks, you could get statements online too. Though again, most only go back a certain number of years.

I am not aware of any credit card company charging the client to get old statements, but you never know.

Keep your paycheck stubs until you receive your W-2 forms, which is typically in January of the next year.

Verify they match, then shred the stubs.

Hold on to the W-2 for at least seven years in case of an audit by the IRS.

I realize that as the year progresses, your pay stub will have updated information in the year to date column.

You might think you could toss the old pay stubs as a result.

But if you do and an issue comes up, you will have to do a lot of math to figure out the numbers.

And if you get special bonuses or your paycheck isn’t the same every week, this could make the math a nightmare.

The simplest solution is to just keep paycheck stubs until you get your W2 in the mail.

How long should you keep brokerage statements?

You should keep the monthly or quarterly brokerage financial statements for both retirement and non-retirement accounts until you get your annual statement.

The same holds true for mutual fund statements.

Once your annual brokerage statement is received and matches the monthly and quarterly statements, you can shred the monthly and quarterly statements.

Keep the annual statement until you sell the securities listed on it.

Again, I’m sounding like a broken record here, but you can get access to some statements online, but only up to a certain point.

I remember owning a mutual fund for many years and having to call the mutual fund company for the investment records so I could confirm my cost basis.

It took over a week to get the statements I needed in the mail.

Furthermore, I know that brokers are now required to report cost basis information, but I still like to have a copy for myself.

Call me crazy, but that’s just me. I get rid of them after I have sold out of the investment in question.

When it comes to how long to keep 401k statements, you should follow the plan above.

Keep the quarterly statements until you get your annual statement. If the annual statement looks good, toss the quarterly statements.

You should keep the annual statements until you sell the investments in your 401k plan or roll it over into an IRA or other 401k plan.

On a related note, if you make both deductible and non-deductible contributions to a traditional IRA, you want to keep the records of nondeductible IRA contributions.

When it comes time to withdraw money from these accounts, you want to be able to have record so you are not paying tax twice.

Any records relating to the purchase of your home should be kept until you sell the house.

You should keep records of your mortgage payments until you get the statement in the mail.

And then you want to keep these monthly statements until you get the tax form showing the interest you paid for the year to make sure it matches.

This is because you can write off mortgage interest on your taxes.

Additionally, a portion of any gains you make on the sale of the home can be excluded from your taxes, so by keeping your statements, you have proof of the amounts you paid.

The same goes for any real estate you purchase.

You want to keep the financial documents until you sell the property.

You should keep the invoices and receipts for the money you spend improving your house over the years.

This is because any improvements you make will adjust the cost basis for you, which affects your capital gains when you sell the house.

For example, as of this writing, the capital gains exemption for a couple married and filing jointly is $500,000.

If they bought a house for $250,00 and it is now worth $800,000 they owe capital gains tax on $50,000 of the $550,000 gain.

But if they improved the home over the years and have receipts showing $30,000 in improvements, they are only taxed on $20,000 of the gain.

The bottom line is, when you improve your house, keep the receipts.

For health insurance statements, you want to keep these until you get an annual statement at the end of the year.

You should keep the annual statements for 7 years if you deducted any of the expenses on your taxes.

If you did not deduct the expenses, then you can shred the statements after the year.

However, if the statement was for doctor visits for serious illnesses, injuries, or chronic aliments, you will want to keep these forever.

This is because you may one day go on disability.

By having these medical bills and medical records, you can prove how long you have been dealing with the issues.

The same holds true for lab tests too.

Also, if it turns out your condition is a result of a product you used, you have the proof for legal action.

While the chances of these are slim, it is better to have the records than not.

In the case of house or car insurance, you only need to keep the financial statements until you get your new policy, then you can toss the old papers.

In the case of life insurance however, you should keep that until you cancel the policy or you use it.

It used to be each year that you received a Social Security benefits statement annually updating you on your estimated benefit when you retired.

Now all of this can be found online. It is up to you if you want to print this out or not.

I choose to print it out after I take a few minutes to verify that the amount of income the online statement shows I earned for the previous year matches with what I actually earned.

The reason I print it out is so I have a copy.

If the website is down or there is a glitch and my records are lost, I have a copy.

Keep all income tax returns, deductible receipts, receipts for charitable contributions, and any other tax related records for 7 years.

You probably even want to keep your actual tax returns permanently.

The IRS has 7 years to audit you if they feel that you made an error on your return.

Additionally, the IRS has 6 years to challenge your return if they feel you under reported gross income by 25% or more.

And there is no time limit on how far back you can get audited if the IRS feels that you filed a fraudulent return.

Lastly, you have three years to file an amended return if you made an error and are claiming a refund.

The simple solution is to just keep all of your personal tax records so you never have to worry.

You want to keep all student loan documents until you paid back the loans in full.

At that point you should receive a letter showing proof of a zero balance.

You can then shred the student loan documents but keep the statement showing your loans were paid in full.

And while you are paying off your student loans, keep the monthly statements until you get a year end statement.

If you don’t get a year end statement showing all of your payments for the year, request one so you can shred the monthly statements.

You want to keep business documents for as long as the business is operating.

Even then, you may want to keep all of your records for 5 years after the business ends, just in case the IRS or your state tax authority has any questions.

In terms of business records, this means everything, including:

The more you keep, the less headache it will be to prove something if someone has a question.

You will keep car registration records for as long as you own the car.

And you should keep everything after the sale until you file that year’s tax return.

This is because you never know if you can deduct an expense.

And here is an added tip.

Keep records of oil changes and regular maintenance you perform.

If you decide to sell the car instead of trading it in, you can usually get a higher sale price by having these documents.

This is because it shows the potential buyer how well you maintained the vehicle.

Of course, you need to keep the title information for as long as you own the car so you can sell it trade it in.

Car accident records should be kept for 7 years.

I know this sounds like a long time, but you want to have proof if anything happens to come up.

The last thing you want to do is have to take the time to call up your insurance agent or the police department to have them find the records.

In addition to the above, there are some things that aren’t financial statements, but you might be wondering if you need to hold on to for the long term.

Here are those items, in no particular order:

Now that you know what financial records to keep and what you can get rid of, you can focus on organizing financial documents you plan to keep.

Your first step is to separate your financial statements into 2 piles, a keep pile and a shred pile.

Use the guidelines I outlined in this post for what you should be keeping and for how long.

To save you some time, here is a PDF you can print out with all of the info.

You might think once you have your two piles you are done organizing your financial paperwork.

You have one more organizing step to do.

Take your keep pile and go through it again.

This time, you will make 2 more piles, an active pile and a storage pile.

Here is what you should keep in the active pile, which should be accessible because chances are you will need to get a hold of these from time to time.

Your storage pile is for all of the financial statements you are keeping that are over 1 year old.

In some cases, this won’t apply to everything.

For example, for tax returns, you will want to keep the prior year’s return in the active pile, but everything older than that can go in storage.

And while product manuals are not considered a financial statement, I still included them in this list above because they are important.

If you regularly refer to the manual, regardless of the age of the item, you should keep it in the active file. All others can go into storage.

You can take the shred pile and shred it all yourself or find a local shredding event.

For the most part, you want to shred these documents instead of just throwing them in the trash.

While not everything has sensitive information on it, the peace of mind knowing there is zero chance of identity theft or fraud is priceless.

The next step is properly storing your important documents.

Now that you have cleaned out a bunch of clutter, it is time to do some financial record keeping organization.

You can go a couple of ways here.

Figure out which option is best for you.

For me, I keep all active files as paper copies and everything else digitally.

The exception is product manuals.

I was planning to start downloading PDF copies but didn’t want to be tied to my computer when looking at them.

I find it easier to read through the actual manual than to scan through it on my phone or computer.

Luckily, no matter which option you choose, they both follow the same outline, and storing financial documents isn’t difficult.

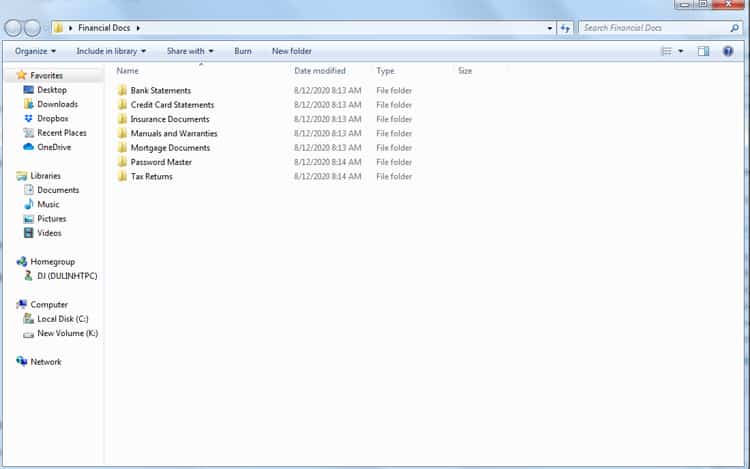

I use use this file organizer for my active file.

I label the folders and put the financial records in their assigned folder.

For digital files, I use a scanner.

You can buy a scanner like this one or you can just use the scan feature if your printer has it.

Just scan your documents, rename them, and insert them into the folders you create.

See the image below as an example.

Just don’t keep the only copy of files on your C drive.

While your C drive is a common place to save files, computers crash all the time.

So be sure you back up your computer using a second hard drive or an external hard drive.

If you are unsure how to do this, here is a simple way to backup your computer on a schedule.

I use a flash drive and I make it a point to back it up monthly just in case.

In fact, I use 2 flash drives.

This way if one gets corrupted, I still have the other one with all my files.

When going digital, just create a folder structure like outlined above.

You will have 2 main folders, active and storage.

Each of these folders will have sub-folders for the documents.

For example, you will have a banking folder, a credit card folder, etc.

To make things easier to transfer over to the storage folder, be sure to include the date in the file name.

Then you can sort by name, highlight all of the old documents to move and move them in bunches.

By organizing the files this way, you can save a lot of time when you have to go back and find specific files.

Hopefully, this guide for how long to keep financial statements helps you to organize your financial statements clear out some of the clutter.

Once you finish going through your files, be sure to keep the most important documents in a fire-proof safe or use a couple of thumb drives.

And as I mentioned earlier, do yourself a favor and buy a shredder to safely destroy those statements you no longer need.

If you don’t feel like shredding the papers yourself, look for shredding events in your area.

Most communities hold these a few times a year.

You drive up to a huge truck that has a shredder in it and toss in your papers.

Of course, you should still buy a shredder too so you can stay on top of discarding files as needed in the future.

I have over 15 years experience in the financial services industry and 20 years investing in the stock market. I have both my undergrad and graduate degrees in Finance, and am FINRA Series 65 licensed and have a Certificate in Financial Planning.

Visit my About Me page to learn more about me and why I am your trusted personal finance expert.